In these cases, the transactions and the period need to be estimated to a specific time period. An example of this is depreciation for equipment expenses, which depends on the estimated number of years which the fixed asset will be functioning and in use. From the perspective of management, these reporting cycles serve as checkpoints to evaluate performance against forecasts and make strategic adjustments. Investors and analysts rely on these reports to track progress and update their valuation models.

Time Period Assumption: Time Period Assumption: GAAP s Framework for Reporting Frequency

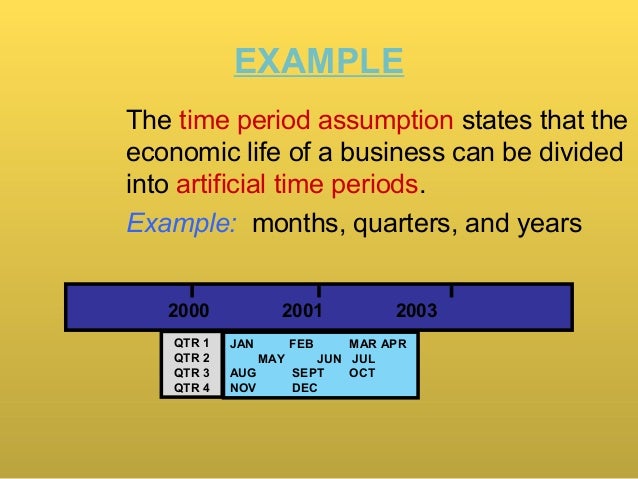

However, the application of this assumption is not without its challenges and nuances, which can be best understood through various case studies. The time period assumption in accounting is a fundamental principle that enables businesses to communicate financial information in a useful and standardized manner. It posits that a business’s complex and ongoing financial activities can be divided into shorter periods, such as months, quarters, or years. This division allows for the presentation of financial statements that are timely, relevant, and comparable across different time frames.

Challenges and Considerations in Applying Time Period Assumption

It allows for the comparison of financial results across different periods, highlighting trends and areas for improvement. For investors and creditors, this assumption provides a consistent basis for analyzing a company’s financial stability and profitability over time. Regulatory bodies and tax authorities also rely on this assumption to ensure compliance with laws and regulations. For example, managers may be tempted to defer expenses or accelerate revenue recognition to meet short-term financial targets, potentially leading to ‘earnings management’ or even fraudulent reporting. From the perspective of financial analysts, the Time Period Assumption is crucial for trend analysis and forecasting.

Usage of Time Periods

The periodicity assumption is important to financial accounting because it allows businesses to show current performance to investors and creditors for shorter periods of time. Hence, income is not the same as cash collections and expense is different from cash payments. Under accrual basis, revenues and expenses are recognized when they occur regardless of when the amounts are received or paid. So, despite the machine being a single, long-term purchase, the periodicity assumption allows the company to split the cost of this asset over the periods in which it’s used.

- Investors and creditors, on the other hand, rely on periodic financial reports to assess the company’s financial health and make investment or lending decisions.

- The time Period assumption is a fundamental concept in accounting that facilitates the accurate and consistent reporting of financial activities.

- Without it, comparing and analyzing financial statements over time would be nearly impossible, as there would be no consistent basis for measurement.

- This method ensures that the revenue is matched with the period in which the service was actually performed, providing a clearer picture of the company’s financial activities during that time.

- Businesses and other economic entities compile and record transactions using one of the several accounting bases that best meet their needs and preferences.

The Intersection of Time and Revenue Recognition

This principle dictates that the complex and continuous economic activities of a business are divided into artificial time periods for the purpose of providing timely information to users. The rationale behind this is the need for regular information to make informed decisions, despite the fact that business activities do not align neatly with calendar periods. One of the benefits is that it allows companies to break down expenses and revenues by months or quarters, which can help make business decisions like forecasting future earnings. However, there are also some disadvantages, such as how too many assumptions made about revenue and expenses over shorter periods may lead to losing important information. It’s also possible that these assumptions can make it difficult for readers who are unfamiliar with how they work in financial statements.

Company

The going concern principle, also known as continuing concern concept or continuity assumption, means that a business entity will continue to operate indefinitely, or at least for another twelve months. The two accounting periods usually followed are the Calendar Accounting Period and the Fiscal Accounting Period. In addition, required to file if the company spends gasoline expenses for her personal trips, then the amount paid for the gasoline should also be treated as a withdrawal of resources by the owner instead of a business expense. For example, you would express the cost of a purchase in dollars, rather than units of time or amount of effort.

The time period assumption allows the company to recognize revenue and expenses related to the project incrementally. This is often done using the percentage-of-completion method, where revenue is recognized based on the project’s progress, providing a more accurate picture of financial performance over specific time frames. The concept of time plays a pivotal role in the recognition of revenue, serving as a fundamental axis upon which the entire edifice of accrual accounting is constructed. This narrative is guided by the realization principle, which stipulates that revenue should be recognized when it is earned, regardless of when the cash is received. However, the temporal dimension introduced by the time period assumption adds layers of complexity to this seemingly straightforward principle.

This flexibility allows businesses to align their financial reporting with seasonal business patterns, providing a clearer picture of financial performance and a more accurate basis for forecasting. The time period assumption plays a pivotal role in financial reporting by providing a temporal framework that aligns with the accrual basis of accounting. It ensures that financial information is presented in a manner that is both meaningful and comparable, supporting various stakeholders in their decision-making processes.

Adherence to this assumption ensures transparency and fairness in financial reporting, which is essential for maintaining trust among investors, regulators, and other stakeholders. While the time period assumption facilitates regular reporting and comparison, it requires careful application and consideration of the business’s unique circumstances. Accountants and analysts must exercise judgment and consider qualitative factors alongside the quantitative data to provide a true and fair view of a company’s financial performance. To illustrate these challenges, consider a construction company that begins a multi-year project.

The first reason is that many businesses have very different levels of activity during certain parts of the year, and it would not be accurate to report all revenues and expenses for each month in full detail. The matching principle states that each revenue recorded should be matched with the related expenses at the same time. The Meta company provides services valuing $2,500 to Beta company during the first quarter of the year.