Proper documentation ensures that you maintain a clear record for future reference and auditing purposes. The reconciliation statement allows the accountant to catch these errors each month. The company can now take steps to rectify the mistakes and balance its statements.

HighRadius Named an IDC MarketScape Leader for the Second Time in a Row For AR

- Using cloud accounting software, like Quickbooks, makes preparing a reconciliation statement easy.

- If you find any errors or omissions, determine what happened to cause the differences and work to fix them in your records.

- We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources.

- After adjusting the balances as per the bank and as per the books, the adjusted amounts should be the same.

- You can also opt to use a simple notebook or spreadsheet for recording your transactions.

A bank may charge an account maintenance fee, typically withdrawn and processed automatically from the bank account. When preparing a bank reconciliation statement, a journal entry is prepared to account for fees deducted. Consider an accounting team at a mid-sized company that needs to perform bank reconciliation on a monthly basis. This task is essential to ensure that their financial records are accurate and up-to-date. A bank reconciliation should be prepared periodically to ensure accurate financial records. This practice is essential for maintaining the financial health and integrity of your business.

Would you prefer to work with a financial professional remotely or in-person?

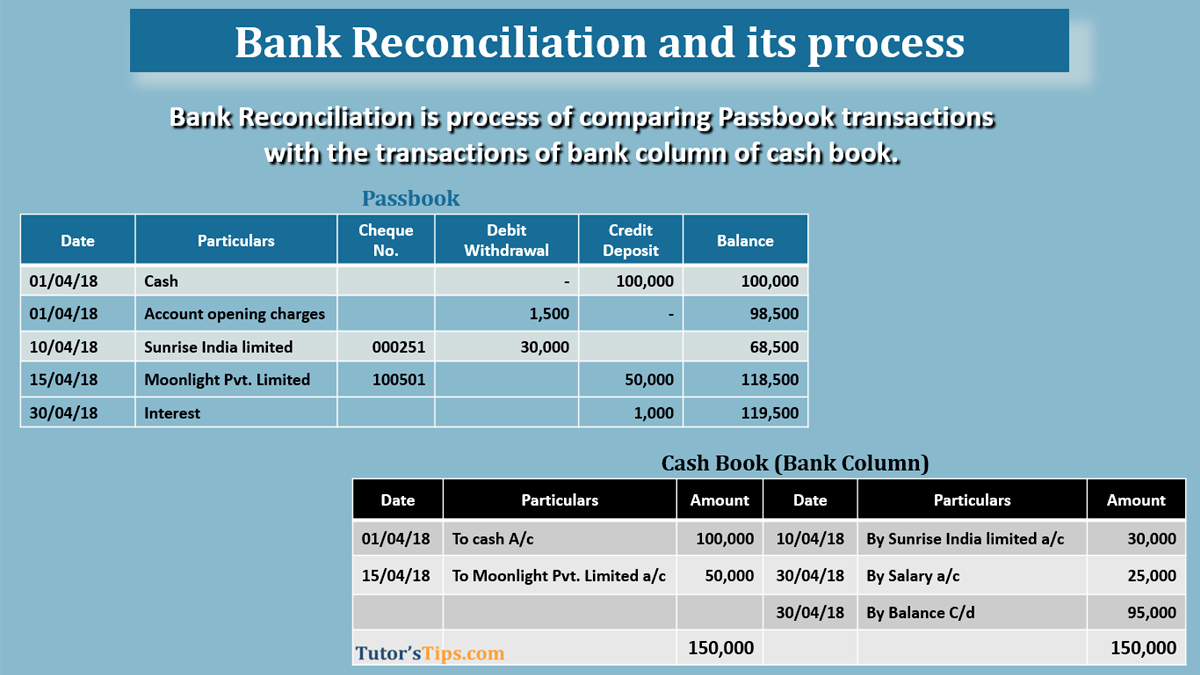

Check that your financial transaction records include all payments and deposits for the transaction period, as well as the final balance. By comparing the two statements, Greg sees that there are $11,500 in checks for four orders of lawnmowers purchased near the end of the month. These checks are in transit, so they haven’t yet been deposited into the company’s bank account. He also finds $500 of bank service fees that hadn’t been included in his financial statement. How you choose to perform a bank reconciliation depends on how you track your money.

Identify Discrepancies

Once you’ve figured out the reasons why your bank statement and your accounting records don’t match up, you need to record them. If you do your bookkeeping yourself, you should be prepared to reconcile your bank statements at regular intervals (more on that below). If you work with a bookkeeper or online bookkeeping service, they’ll handle it for you. In cases where you discover discrepancies that cannot be explained by your financial statements, it’s best to contact your bank.

Taking the time to perform a bank reconciliation can help you manage your finances and keep accurate records. This relatively straightforward and quick process provides a clear who should prepare a bank reconciliation? picture of your financial health. Consider reconciling your bank account monthly, whether you set aside a specific day each month or do it as your statements arrive.

To reconcile means to “make one view or belief compatible with another.” In accounting, that means making your account balances equal to one another. More specifically, a bank reconciliation means balancing your bank statements with your bookkeeping. Match the deposits in the business records with those in the bank statement. Consider performing this monthly task shortly after your bank statement arrives so you can manage any errors or improper transactions as quickly as possible. To create a bank reconciliation, you will need to gather your bank statements and reconcile them with your accounting records (ledger).

The reconciliation process also helps you identify fraud and other unauthorized cash transactions. As a result, it is critical for you to reconcile your bank account within a few days of receiving your bank statement. We strongly recommend performing a bank reconciliation at least on a monthly basis to ensure the accuracy of your company’s cash records.

Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own.

The reconciliation of bank statements is a critical step in maintaining accurate financial records for any business, ensuring that the company’s accounting records are up-to-date and accurate. By reconciling bank statements regularly, business owners can identify any missing or duplicate transactions, bank errors, or fraudulent activity early on, before they pose significant challenges. Reconciliations are typically done on a monthly basis to ensure that all deposits, withdrawals, and bank fees are accounted for. Discrepancies between a bank statement and book balance are commonplace, but businesses must account for each one and adjust the general ledger accordingly. Performing a regular bank reconciliation enables a business to locate any missing funds, prevent fraud, and verify the cash flow on its balance sheet.

Uncleared checks are checks that have been issued but not yet cashed by the recipient. These can create discrepancies between your bank statement and your cash book. For example, if you issue a check to a supplier at the end of the month, it might not clear until the following month.